How much does a 4-point inspection cost?

How much does a 4-point inspection cost?

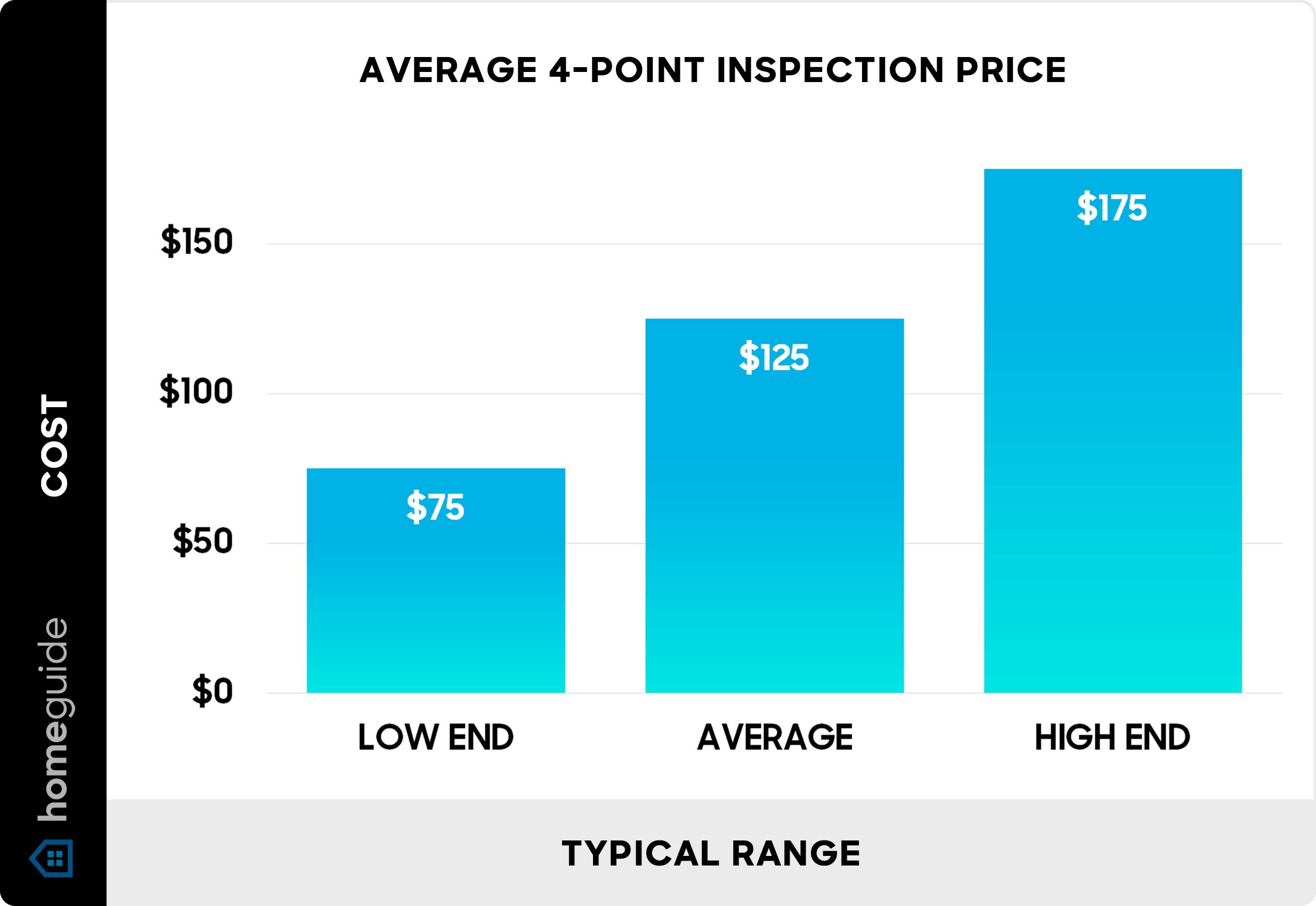

$75 – $175 average inspection cost

4-point inspection cost

A 4-point inspection costs $75 to $175 on average, with most homeowners paying around $125 for this essential insurance requirement. This specialized inspection focuses on the four critical systems insurance companies care about most: your roof, electrical, plumbing, and HVAC systems. When bundled together, a wind mitigation and 4-point inspection costs $125 to $325.

| National Average Cost | $125 |

| Minimum Cost | $50 |

| Maximum Cost | $300 |

| Average Range | $75 to $175 |

What is a 4-point inspection?

A 4-point inspection gives a homeowners insurance company insight into the current condition of a house through an in-depth examination and evaluation of its four major systems: roofing, electrical, plumbing and HVAC. Unlike a comprehensive home inspection, this focused assessment is specifically designed for insurance purposes.

These systems will likely require expensive repairs during use. Insurance companies use this information to evaluate their risk and determine whether to offer coverage and at what premium.

When do you need a 4-point inspection?

If your home is more than 20 years old, most insurance companies require a 4-point inspection before issuing a new homeowners policy. However, requirements vary by insurance company and state. Common scenarios requiring 4-point inspections include:

Purchasing an older home: When you buy an older home, you will need a 4-point Inspection before obtaining homeowners insurance.

Policy renewal: Existing homeowners may need updated inspections when renewing coverage, especially if their previous report is over 3 to 5 years old.

Switching insurance companies: When you change insurance companies, the new insurer typically requires a current inspection report, even if you had one for your previous company.

Claims history concerns: Insurance companies may require inspections for homes with previous claims or those in high-risk areas.

4-point home inspection cost factors

The cost of your four-point inspection depends on several factors:

Home age and condition: Older homes may require more thorough evaluation, especially those over 20 or 30 years old where insurance companies typically mandate these inspections.

Property size: Larger homes take more time to inspect, which can increase costs. Most inspectors charge a flat fee, but exceptionally large properties may incur additional charges.

Location and market demand: Pricing varies significantly across different regions of the United States, with inspectors in coastal areas typically charging more due to increased hurricane and storm risks. Major cities with higher demand also have higher rates.

Inspector qualifications: A state licensed home inspector or contractor must do the inspection and sign the report, which affects pricing based on their certification level and experience.

Bundled services: Many companies offer discounts when combining 4-point inspections with other services.

Wind mitigation and 4-point inspection cost

Many homeowners need both inspections to satisfy insurance requirements and maximize savings. Companies often offer both inspections at discounted rates when bundled together or at reduced prices when added to full home inspections.

The table below shows what you can expect to pay when bundling services, which often provides the best value for homeowners.

| Service combination | Average cost |

|---|---|

| 4-point inspection only | $75 – $175 |

| Wind mitigation only | $75 – $175 |

| Both inspections together | $125 – $325 |

| Both with full home inspection | $350 – $650 |

Why get both inspections together?

Besides the potential cost savings, there are several benefits to bundling 4-point inspection and wind mitigation inspection services together:

Time efficiency: Both inspections can be completed in a single visit, typically taking 2 to 3 hours total.

Complete documentation: Having both reports ensures you meet all insurance requirements and can claim available discounts.

Insurance benefits: With minimal wind mitigation features in place, the inspection will pay for itself in the first year. Credits can go up to the maximum savings of 88% off the hurricane/wind premium.

What's included in a 4-point inspection?

Each of the four main systems receives focused attention during the inspection process.

Plumbing system review

Plumbing evaluation covers water supply and drainage systems:

Pipe materials and condition

Water heater age and type

Signs of leaks or water damage

Water pressure and flow

Drainage functionality

Electrical system assessment

The electrical inspection focuses on safety and code compliance, examining:

Main electrical panel and breakers

Wiring type and condition

Grounding systems

GFCI protection

Signs of overloading or hazards

Common electrical issues that can cause a home to be denied insurance during a 4-point inspection include outdated or hazardous electrical panels.

Roofing system evaluation

A home inspector will visually inspect your roof, looking for any signs of damage or deterioration in roofing materials and shingles. The inspector will also check the soundness of the roof construction both inside and out and note the age of the roof.

Areas examined include:

Roof covering type and condition

Age and remaining useful life

Signs of leaks or damage

Missing or deteriorated shingles

Structural integrity

HVAC system inspection

The inspector will look for obvious signs of leakage and issues with the ventilation system and check to make sure hot and cold air comes out of the vents.

The HVAC assessment includes:

Heating and cooling equipment condition

Ductwork integrity

Air filtration systems

Proper installation and operation

Age and maintenance status

4-point inspection vs. full home inspection

Unlike a full home inspection, a 4-point inspection only covers key components and systems, including a home's roof, HVAC system, plumbing, and electrical. A full home inspection costs more but also includes appliances, the foundation, windows and doors, pests, and other factors.

| Feature | 4-point inspection | Full home inspection |

|---|---|---|

| Cost | $75 – $175 | $300 – $600 |

| Duration | 45 – 90 minutes | 2 – 4+ hours |

| Systems covered | 4 major systems | All visible systems |

| Report length | 2 – 4 pages | 40 – 80 pages |

| Purpose | Insurance requirement | Buyer protection |

Avoid being shortsighted in your biggest purchase, which is likely to be your home. Considering the big picture, home inspections are relatively inexpensive and can prevent you from buying a hazardous home.

What can cause a 4-point inspection to fail?

Several conditions can result in an unfavorable inspection report that may lead to insurance denial or required repairs. Common failure points include:

Roof issues: A roof with any leaks at all or a roof more than 15 years old may cause inspection failure. An estimated additional roof life of 5-years is the usual standard for a roof to be acceptable.

Electrical problems: Outdated panels, aluminum wiring, or code violations can result in coverage denial.

Plumbing concerns: Polybutylene pipes, significant leaks, or very old, galvanized plumbing may be problematic.

HVAC deficiencies: Lack of an installed heating system may be an issue. Window A/C units or plug-in portable heaters are not considered "installed."

Insurance company responses to issues

Some insurance providers will not include coverage for problem systems (e.g., water damage with polybutylene plumbing). Others won't write the policy at all.

Companies may:

Require repairs before issuing coverage.

Exclude specific systems from coverage.

Charge higher premiums.

Decline to provide coverage entirely.

4-point inspection FAQs

How long does a 4-point inspection take?

Most 4-point inspections take 45 to 90 minutes to complete. The inspector focuses only on the four major systems, making it much faster than a comprehensive home inspection.

How long is a 4-point inspection good for?

A 4-point inspection report is typically valid for up to 1 year. Most insurers now require an inspection from within the past 12 months, especially for new policies. If you switch insurance companies, your new insurer may require a fresh inspection even if your current report is still within the accepted timeframe.

Who can perform a 4-point inspection?

A licensed home inspector, general contractor, residential contractor, or building contractor who is certified in the state where the inspection takes place must perform the inspection and sign the report. Insurance companies in most states require that inspectors hold an active state license and, often, additional certifications from recognized organizations such as InterNACHI or the International Code Council.

Do I need both a 4-point inspection and wind mitigation inspection?

Whether you need both a 4-point inspection and a wind mitigation inspection depends on your location and insurance requirements. Four-point inspections are compulsory for older homes, while wind mitigation inspections are completely optional. However, wind mitigation inspections can provide substantial insurance discounts.

How to find the best home inspector near you

Follow these steps to ensure you hire a qualified home inspector near you who meets insurance requirements and provides accurate reporting:

Verify licensing and certifications with your state's regulatory board.

Ask for references from recent clients and insurance agents.

Confirm they use current, insurance-accepted forms and reporting standards.

Check online reviews and ratings on Google and HomeGuide.

Ensure they carry professional liability insurance.

Compare pricing but don't choose based solely on the lowest cost.

Ask about turnaround time for report delivery.

Questions to ask a home inspector

Use these questions to evaluate potential inspectors:

Are you licensed and insured in this state?

How long have you been performing 4-point inspections?

What's included in your inspection fee?

How quickly will I receive the report?

Do you offer package deals with wind mitigation or full inspections?

Can you provide references from recent clients?

What happens if the insurance company has questions about your report?

Do you offer any guarantees on your work?

Are you familiar with my specific insurance company's requirements?

Using our proprietary cost database, in-depth research, and collaboration with industry experts, we deliver accurate, up-to-date pricing and insights you can trust, every time.